Rate cuts could help Black families but barriers remain

By Miriam Musa

Rolling Out

https://rollingout.com/

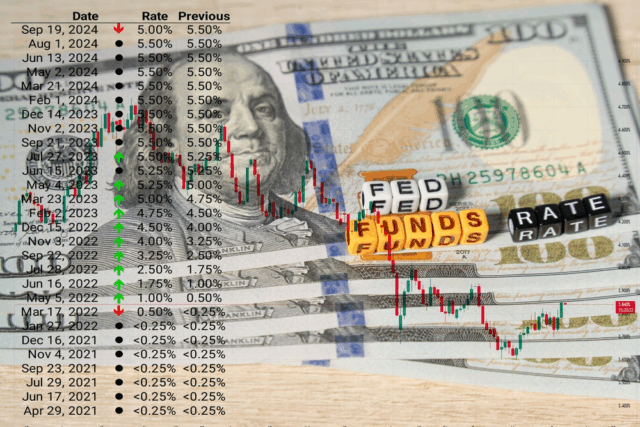

Wall Street woke up feeling optimistic this morning after President Trump announced his pick for a new Federal Reserve Governor — someone the markets believe will push for lower interest rates in the coming months. Stock futures jumped as investors started calculating what cheaper money could mean for corporate profits and economic growth.

But while traders are celebrating on Wall Street, the real question is what this potential shift means for everyday Black families trying to build wealth, buy homes, and start businesses. Two expected rate cuts before year’s end could open doors that have been locked for too long, but only if the benefits actually reach the communities that need them most.

What dovish really means for your wallet

When Federal Reserve officials take a dovish stance, they’re prioritizing economic growth over keeping inflation under tight control. In practical terms, this translates to lower interest rates across the board — on mortgages, car loans, business loans, and credit cards.

For Black families who have been priced out of homeownership by sky-high mortgage rates, this could be the break they’ve been waiting for. That house that seemed impossibly expensive six months ago might suddenly become affordable with a rate that’s two percentage points lower.

Small business owners in Black communities could finally access the capital they need to expand without interest payments that eat up all their profits. Whether you’re trying to open a restaurant, launch a beauty supply store, or grow a consulting business, lower rates mean more of your revenue stays in your pocket instead of going to the bank.

The opportunity gap persists

Here’s where things get complicated, though. Even when interest rates drop across the economy, Black borrowers consistently face higher costs and more frequent rejections than white applicants with identical credit profiles. This isn’t accidental — it’s the result of systemic discrimination in lending that persists despite decades of civil rights laws.

Lower rates don’t automatically mean equal access. If banks continue their discriminatory practices, a rate cut environment could actually widen the racial wealth gap by making it easier for already-privileged families to access cheap credit while maintaining barriers for everyone else.

The Federal Reserve can lower rates, but it can’t force banks to lend fairly. That requires strong enforcement of fair lending laws and ongoing pressure on financial institutions to serve all communities equally.

Wall Street’s excitement tells a story

The market’s immediate positive reaction to Trump’s Fed nominee isn’t just about cheaper borrowing costs — it’s about policy predictability. Investors believe this pick signals a commitment to rapid economic growth, even if that means accepting slightly higher inflation.

If the Fed delivers those two rate cuts before December, we could see stock markets continue climbing, more investment flowing into housing and technology, and corporations feeling confident enough to expand and hire. That economic activity tends to create opportunities, but historically those opportunities haven’t been distributed equally.

Real wealth building opportunities

For Black families positioned to take advantage, lower rates could create genuine wealth-building momentum. First-time homebuyers who have been saving and waiting might finally find their entry point into property ownership — the foundation of generational wealth for most American families.

Entrepreneurs with solid business plans but limited capital could secure loans that actually make sense financially. Instead of borrowing at rates that guarantee failure, business owners could access credit that allows their ventures to thrive and grow.

Black investors who have been building portfolios could see significant gains if markets continue their upward climb. While investing always involves risk, lower rates typically drive money toward stocks and other growth assets that can build wealth over time.

The inflation concern

Lower interest rates come with a potential downside that could hit Black households particularly hard. If rate cuts overheat the economy and drive up inflation, the cost of essentials like groceries, gas, and rent could surge.

Black families typically spend a higher percentage of their income on basic necessities, making them more vulnerable to inflation than households with more discretionary income. What looks like an economic boost could turn into a financial squeeze if prices rise faster than wages.

There’s also the possibility that rate cuts signal underlying economic weakness. Sometimes the Fed lowers rates not because the economy is strong, but because it’s worried about recession. Lower rates might provide temporary relief while bigger problems brew beneath the surface.

Strategic moves to consider

If you’re thinking about major financial decisions, now might be the time to act strategically. Locking in fixed-rate loans before rates become unpredictable could save thousands of dollars over time. Whether it’s a mortgage, business loan, or even refinancing existing debt, securing favorable terms now provides protection against future uncertainty.

This is also an ideal time to attack high-interest debt aggressively. If borrowing costs are falling, the gap between what you’re paying on credit cards and what you could pay on new loans is getting wider. Consolidating or paying down expensive debt frees up money for wealth-building activities.

For those with some capital to invest, lower rates often drive asset prices higher. Real estate, stocks, and other investments that generate returns over time become more attractive when safe savings accounts are paying almost nothing.

The bigger picture matters

Beyond individual financial decisions, this Fed nomination represents a broader philosophy about how the economy should work. The choice between prioritizing growth versus controlling inflation affects every aspect of American life, from job availability to housing costs to retirement planning.

For Black communities that have been systematically excluded from wealth-building opportunities, Fed policy can either open doors or keep them closed. Lower rates create possibilities, but realizing those possibilities requires fair access to credit, protection from discrimination, and support for building financial literacy and business skills.

What happens next

The Fed’s next moves will ripple far beyond trading floors and corporate boardrooms. For Black families, the question isn’t just whether money will get cheaper — it’s whether the financial system will finally start working for everyone.

Rate cuts create opportunities, but taking advantage of those opportunities requires preparation, knowledge, and persistence. It means building credit, saving for down payments, developing business plans, and staying informed about changing market conditions.

Bottom line? Trump’s Fed nominee pick has Wall Street excited about the possibility of cheaper money and faster growth. For Black families and entrepreneurs, this could represent a real chance to access credit, buy homes, and build businesses that create generational wealth. But only if we’re prepared to seize these opportunities and demand fair treatment from lenders who have historically kept these doors closed. The tools for wealth building might be getting more accessible — now it’s up to us to use them effectively.